Returns and fear

When markets start to fall, the temptation to lighten the portfolio's equity component can be especially strong. Determining whether this is a clever idea is difficult because part of the answer depends on how much you can afford a large short-term loss. In general, however, those who can afford to wait for the recovery of the indices are rewarded.

This is what T. Rowe Price, an asset management company, did by observing what happened, historically, in the months following a peak in volatility. Although past performance is no indication of the future, over an 18-month horizon, U.S. stock returns have turned out to be markedly superior when preceded by a spike in investor fear.

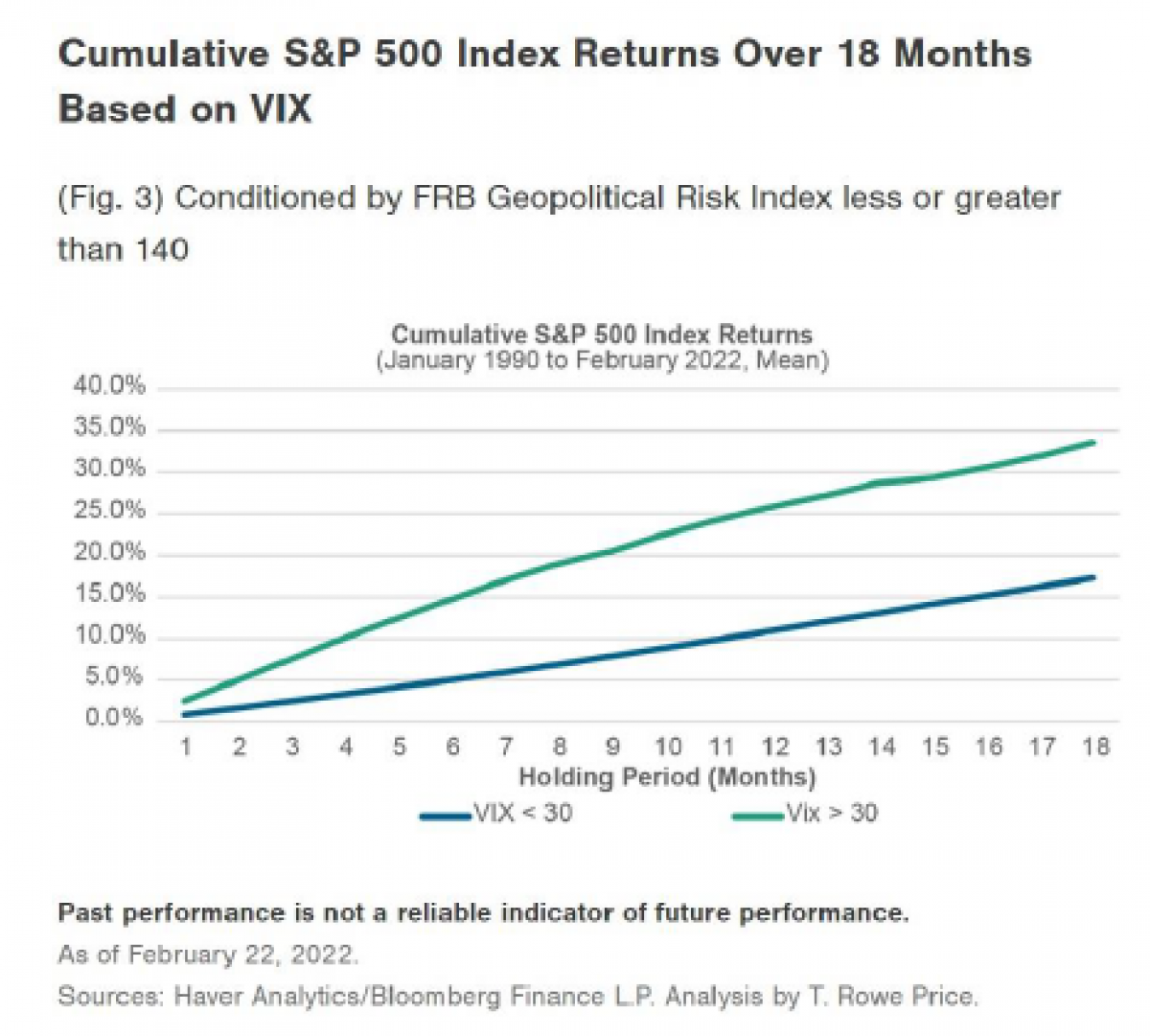

For example, let’s review the performance of the New York Stock Exchange in two scenarios between 1990 and late February 2022. In the first, the VIX index — which indicates how much investors expect a stock to fall on the New York Stock Exchange a month later — was below 30 points at the initial time of the observation. In the second case, the scenario was that the stress of market participants is greater, and the VIX was beyond this threshold.

Haver Analytics/Bloomberg Finance. Analysis by T. Rowe Price.

Haver Analytics/Bloomberg Finance. Analysis by T. Rowe Price.

What emerged confirms how, on average, a spike in volatility tends to be followed by superior performance. The yields of the New York Stock Exchange, in the scenario in which the VIX was at the initial observation point above 30 points, were approximately double when compared to the other scenario at the end of the following 18 months. In addition, the probability of posting a positive cumulative performance over 12 months was greater than 90% when the VIX starting point was above 30. The percentage approaches 80% in the less strenuous initial scenario.

This observation seems to justify a more patient stance in the face of volatility or a bold buying approach in times of greatest tension.

This analysis suggested that volatility spikes are not a good signal to sell because returns tend to be above average in the 18 months following a volatility spike. Markets naturally tend to rebound after being oversold during the correction.

Investors need to stay disciplined and not panic sell, and those who do often only manage to lock in losses. Market timing, the practice of trying to buy and sell by promptly interpreting the current situation, is always difficult, even more so in times of severe stress and turbulence, because an investor who sells and moves into liquidity could re-enter the market late.

Conversely, periods of higher volatility can potentially provide investors with good longer-term entry points.

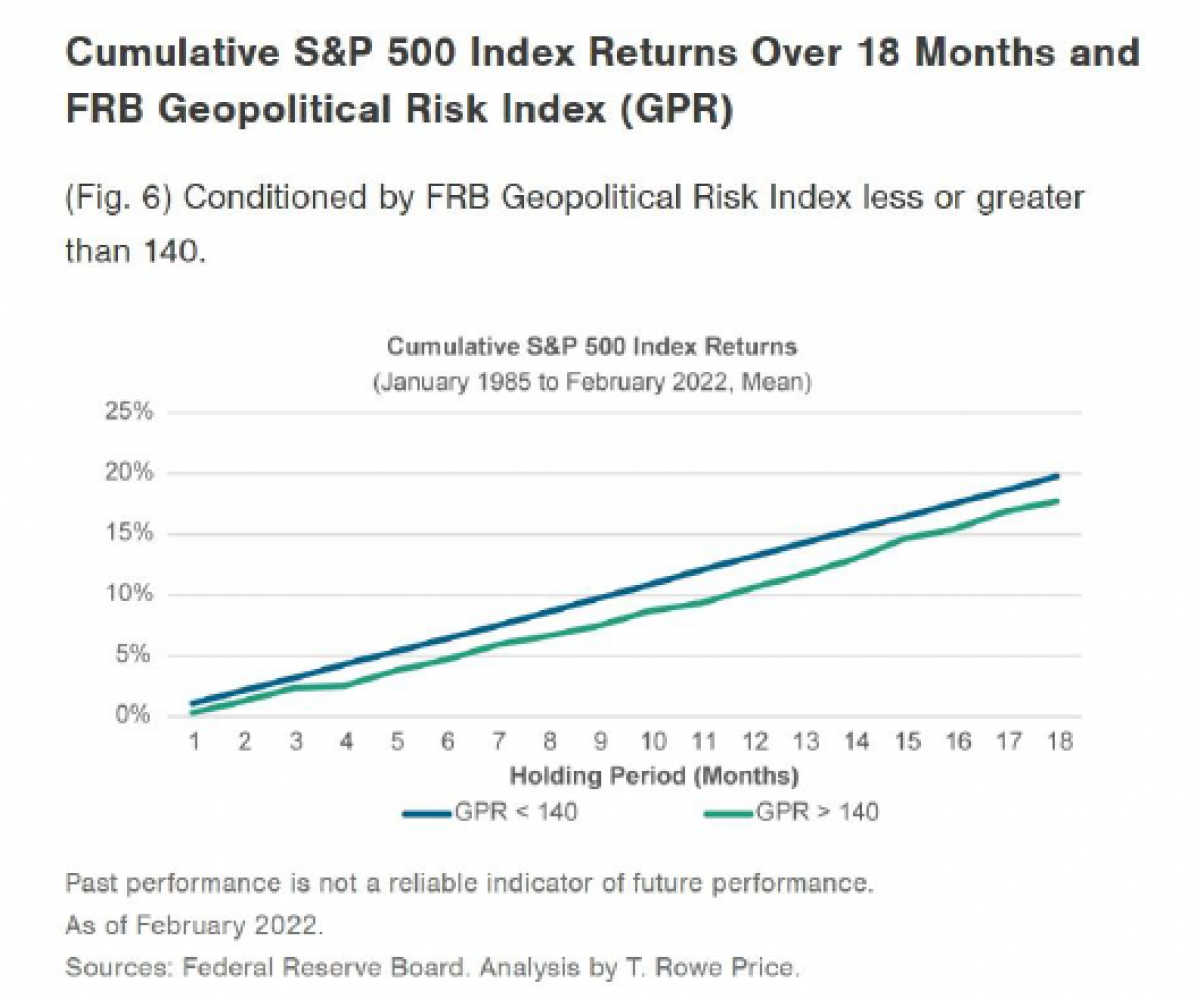

The analysis of the fear indicated by the VIX has proved to be a good anticipatory signal for the subsequent recovery of the market. On the other hand, much less so is the index on geopolitical tension elaborated by the Federal Reserve. The organization’s Federal Reserve Board Geopolitical Risk Index indicator depends on the results of an automated text search in the electronic archives of 10 newspapers, starting from 1985.

After reaching a peak, it does not show recoveries by the U.S. stock market in the following 18 months: there is no historical evidence that an increase in geopolitical risks could lead to strong forward returns.

The reason periods of heightened geopolitical risk are not typically good entry points for investors may be that few have insider knowledge of the duration or severity of geopolitical developments, so it may not be wise to use a geopolitical risk indicator such as a market timing signal.

Comments

Comments

Related Articles

Copyright © 2026 - All Rights Reserved

ISSN 2768-198X

List

Add

Please enter a comment